Unpredictable

Complexity versus tidy models. Spoiler alert: complexity wins (every time)

Introduction

As someone with an undergraduate degree in economics (and a healthy heaping of statistics on top of that), I have always been fascinated by the intricate dance of cooperative agent behavior, and the seemingly magical predictions made by social scientists. Initially, I was intrigued by the seeming elegance of economic and econometric theories and the promise they held for explaining and predicting future behavior. Over time, I began to notice the limitations and inconsistencies in even the best predictions. Thus, a seed of doubt emerged in my mind about the scientific rigor of many social sciences (economics in particular).

My career took a different path when I became a software developer, working extensively with machine learning applications. Over the years, I have been involved in many projects that required building predictive models. This experience gave me a perspective on the challenges of prediction and the complexity of the systems we try to model. The more I worked with machine learning models and approaches, the more I realized how difficult it is to predict outcomes accurately, even with vast amounts of data and sophisticated algorithms. This hands-on experience only served to enhance my skepticism about the predictive power of economics.

My interest in complex systems and chaos theory was ignited after reading James Gleick's 1988 book, "Chaos: Making a New Science." This book opened my eyes to the profound unpredictability inherent in complex systems. Gleick's exploration of chaos theory revealed how small changes in initial conditions could lead to dramatically different outcomes, a phenomenon known as the butterfly effect. Over the years I also came to discover the works of Scott Page, Donella Meadows, and Jerry Gaus.

These concept resonated deeply with my sense of how the world around me seems to work. ( You can develop a relatively good understanding of complex systems via this collection of books. ) and it led me to question the fundamental assumptions underlying economic predictions. My intent here is to explore the impossibility of predicting outcomes in complex systems and what that means for everything from economics to climate science.

Understanding Complex Systems

Complex systems are pervasive in our world, encompassing phenomena as diverse as weather patterns, ecosystems, ants, the human brain, and economies. These systems are characterized by their intricate interdependencies and non-linear interactions among components. Unlike simple systems, where cause and effect are straightforward and predictable, complex systems exhibit behaviors that can be counterintuitive and unpredictable. The interactions within these systems lead to emergent properties, where the whole is greater than the sum of its parts. Understanding these properties requires a shift from linear thinking to a more holistic perspective.

One of the defining features of complex systems is their sensitivity to initial conditions. This concept, often illustrated by the butterfly effect, posits that a small change in the starting state of a system can lead to vastly different outcomes. This sensitivity makes long-term prediction extremely difficult, if not impossible. Even with detailed knowledge of the initial state and the governing rules, the inherent unpredictability of these systems remains. This unpredictability is not due to a lack of understanding or data but is a fundamental characteristic of complex systems.

An equally crucial aspect of complex systems is their non-linearity. In a linear system, changes in inputs lead to proportional changes in outputs. However, in a non-linear system, small changes in input can result in disproportionately large or small changes in output. This non-linearity can lead to phenomena such as tipping points, where a small perturbation causes a sudden and dramatic shift in the system's behavior. Non-linearity also means that feedback loops, both positive and negative, play a significant role in shaping the system's dynamics. These feedback loops can amplify or dampen the effects of changes, further complicating prediction.

The concept of emergence is central to understanding complex systems. Emergent properties arise from the interactions of the system's components and cannot be predicted by examining the components in isolation. For example, the behavior of an economy cannot be fully understood by studying individual consumers and firms; it emerges from their interactions and the rules governing these interactions. This emergent behavior can lead to unexpected and often unpredictable outcomes. Recognizing and studying these emergent properties is key to gaining insights into complex systems, but it also underscores the limitations of traditional reductionist approaches to prediction and control.

The Nature of Predictability

Predictability is a concept that is intuitively understood in the context of simple systems but becomes profoundly complex when applied to complex systems. In simple systems, predictability is straightforward: given a set of initial conditions and governing laws, the future state of the system can be determined with high accuracy. Classic examples include the motion of planets, billiard balls, or the behavior of pendulums, where well-defined physical laws allow for precise predictions. These systems exhibit a linear relationship between cause and effect, making them deterministic and predictable.

However, complex systems operate under fundamentally different principles. One of the key challenges in predicting complex systems is their sensitivity to initial conditions. This sensitivity means that even minute differences in the starting state of the system can lead to vastly different outcomes. This concept is famously encapsulated in the butterfly effect, which suggests that the flap of a butterfly's wings in Brazil could set off a tornado in Texas. This sensitivity makes long-term predictions virtually impossible, as it requires perfect knowledge of the initial conditions, which is often unattainable in practice.

Non-linearity further complicates predictability in complex systems. Unlike linear systems, where changes in inputs produce proportional changes in outputs, non-linear systems can respond in unpredictable ways. Small inputs can produce disproportionately large outputs, and vice versa. This non-linearity can lead to phenomena such as tipping points, where a small change triggers a significant shift in the system's state. Such behavior is often observed in financial markets, ecosystems, and climate systems, where minor perturbations can lead to major upheavals. Non-linearity thus introduces a level of unpredictability that defies simple cause-and-effect reasoning.

Chaos theory provides a framework for understanding the inherent unpredictability of complex systems. It reveals that even deterministic systems can exhibit chaotic behavior, where long-term prediction is impossible despite the system being governed by deterministic laws. This paradoxical notion – that deterministic systems can be unpredictable – underscores the limits of traditional scientific approaches to prediction. Chaos theory shows that unpredictability in complex systems is not just a matter of insufficient data or computational power but a fundamental characteristic of the systems themselves.

Moreover, the concept of emergence adds another layer of unpredictability. Emergent properties arise from the interactions of the system's components and cannot be predicted by analyzing the components in isolation. These properties are a hallmark of complex systems, where the whole exhibits behaviors and characteristics that are not evident from the parts. For instance, the collective behavior of an ant colony or the dynamics of an economy cannot be deduced by studying individual ants or economic agents alone. Emergence highlights the limitations of reductionist approaches and the need for holistic analysis to understand and predict the behavior of complex systems.

Case Study: Global Warming

Global warming, as a facet of climate change, offers a compelling case study in the challenges of predicting outcomes within a complex system. The Earth's climate system is highly intricate, governed by interactions among the atmosphere, oceans, land surfaces, and living organisms. These components interact in non-linear ways, leading to emergent behaviors that complicate any long term predictions. Despite the sophisticated climate models developed by scientists, accurately forecasting the precise impacts of global warming over long time scales remains fraught with massive uncertainty.

Aside: this example is not meant to dispute the fact that the planet is getting warmer, it is. It does offer a rational reason to be skeptical about the accuracy long term claims (i.e. what will the climate look like in 2100 or 2200). I strongly favor efforts to reduce the global dependence on fossil fuels, I’m just not willing to say with certainty what the global climate will look like for more than a few years (3-5?) out.

One of the primary difficulties in predicting global warming outcomes is the sensitivity of the climate system to initial conditions. Small changes in atmospheric composition, ocean temperatures, or land use can set off feedback loops that amplify or dampen warming trends. For example, the melting of polar ice reduces the Earth's albedo, causing more solar energy to be absorbed and further accelerating ice melt. Such feedback mechanisms can lead to tipping points, where gradual changes suddenly trigger significant and possibly irreversible shifts in the climate. This sensitivity underscores the challenges in making precise long-term predictions about climate change.

Non-linearity is another significant factor complicating global warming predictions. The relationships between greenhouse gas emissions, temperature increases, and their impacts are not linear. Small increases in carbon dioxide concentrations can have outsized effects on global temperatures, and these temperature changes can, in turn, lead to disproportionate impacts on weather patterns, sea levels, and ecosystems. The non-linear nature of these relationships means that predicting specific outcomes, such as the frequency and intensity of extreme weather events, is inherently difficult. This non-linearity also implies that mitigation efforts might not produce proportional benefits, adding another layer of complexity to any attempt to construct a meaningful climate policy.

Moreover, the concept of emergence is vividly illustrated in the context of global warming. Emergent properties of the climate system arise from the complex interactions of its components and are not predictable by studying individual elements in isolation. For instance, regional climate patterns, such as monsoon systems or ocean currents like the Gulf Stream, result from the interplay of various factors and can exhibit unexpected changes in response to global warming. These emergent behaviors complicate our ability to forecast regional climate impacts accurately and highlight the limitations of reductionist approaches. Understanding and predicting the full scope of global warming's effects require a holistic view of the climate system, acknowledging its complexity and inherent unpredictability.

The sensitivity to initial conditions, non-linearity, and emergence within the climate system all contribute to the inherent unpredictability of long-term climate forecasts. While climate models provide valuable insights and help guide policy decisions, they also underscore the limitations of our predictive capabilities. Recognizing these challenges is crucial for developing adaptive and resilient strategies to address the multifaceted impacts of global warming.

Economies as a Complex System

Economies, like climate systems, are a prime example of a complex system. An economy is driven by countless variables, including human behavior, market dynamics, governmental policies, and global events. These elements interact in non-linear and, in many cases, unpredictable ways, making the task of economic prediction incredibly challenging. While economic models aim to simplify and provide insights into these interactions, they often fall short in capturing the full complexity of the economic landscape. The inherent unpredictability of economic systems raises important questions about the scientific rigor of economics as a discipline.

One of the central challenges in any economic prediction is the sensitivity to initial conditions. Small changes in consumer confidence, interest rates, or commodity prices can lead to significant and sometimes unexpected shifts in the broader economy. For instance, a minor adjustment in monetary policy by a central bank can have far-reaching effects on inflation, employment, and investment. These small initial changes can set off a cascade of reactions, amplifying their impact in unpredictable ways. This sensitivity makes it difficult to foresee the long-term consequences of economic decisions and policies.

Non-linearity further complicates economic predictions. Economic relationships are rarely linear; instead, they often exhibit threshold effects and tipping points. For example, a modest increase in unemployment can lead to a disproportionate drop in consumer spending, which in turn can exacerbate an economic downturn, creating a vicious downward cycle. Similarly, financial markets experience sudden and dramatic shifts due to non-linear dynamics, such as the rapid spread of panic during a financial crisis. These non-linear interactions mean that small perturbations can lead to significant and sometimes catastrophic economic outcomes, challenging the reliability of economic forecasts.

The concept of emergence is also crucial to understanding economics as a complex system. Economic phenomena often arise from the interactions of individual agents, such as consumers, firms, and governments, which cannot be fully understood by examining these agents in isolation. Market trends, bubbles, and crashes are emergent properties that result from the collective behavior of market participants. For example, the 2007-2008 financial crisis emerged from the complex interplay of housing market dynamics, financial instruments, and regulatory environments. These emergent behaviors are difficult to predict and manage, highlighting the limitations of reductionist approaches in economics. Recognizing the emergent nature of economic phenomena underscores the need for holistic and adaptive approaches to economic analysis and policy-making.

Sensitivity to initial conditions, non-linearity, and emergence make long-term economic prediction inherently challenging and call into question the scientific rigor of economic models. While economics purports to provide valuable insights into market dynamics and policy impacts, its predictive power is critically limited by the complexity of the systems it seeks to understand. Acknowledging such limitations seems to be a crucial step befor developing more robust and adaptive economic theories and policies that can better navigate the uncertainties of the real world.

Critique of Economics as a Science

Over my career, I have come to wonder about the classification of economics as a science. At the heart of my concern is a fundamental question of whether economics possesses predictive powers and empirical rigor to the same degree as the natural sciences. Unlike physics or chemistry, where experiments can be controlled and repeated with consistent results, economics deals with human behavior and social interactions, which are inherently variable and unpredictable. This variability introduces a level of uncertainty that challenges the scientific status of economics.

One of my (and others) primary criticisms of economics is its reliance on models that simplify reality to a significant extent. Economic models often rest on assumptions that do not hold true in the real world, such as rational behavior, perfect information, and market equilibrium. While these assumptions make models mathematically tractable, they also strip away the complexities and nuances of actual economic behavior. This simplification can lead to misleading conclusions and failed predictions, as evidenced by the numerous economic crises that have caught economists off guard. The 1997 Asian financial crisis, for example, revealed the limitations of models that failed to account for the interconnectedness and fragility of financial markets. Just ask the guys at Long Term Capital Management.

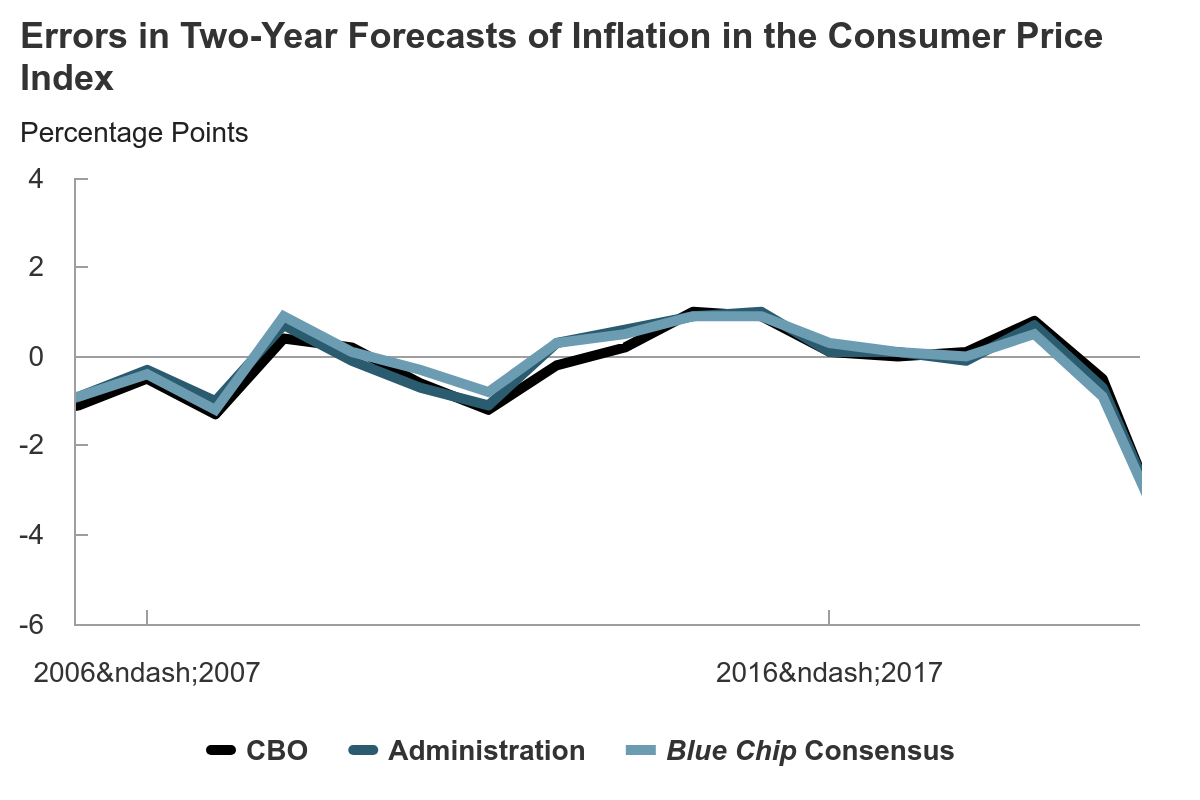

Moreover, the predictive power of economic models is often called into question. Unlike natural sciences, where theories can predict outcomes with a high degree of accuracy, economic forecasts frequently miss the mark. This inconsistency is partly due to the non-linear and emergent nature of economic systems, which are influenced by a multitude of factors, including psychological, social, and political elements. The inability to account for these factors and their interactions leads to predictions that are often no better than educated guesses when trying to go beyond 24 months (see CBO graph below) and sometimes even very wrong inside of the 24 months. This lack of predictive accuracy undermines the claim that economics operates with the same scientific rigor as disciplines like physics or chemistry.

Another critique lies in the methodological approach of economics. While natural sciences rely heavily on empirical testing and experimentation, much of economic analysis is theoretical and model-based. Economists often use historical data to validate their models, but this approach has limitations. Historical data can be incomplete or biased, and past trends do not always predict future behavior, especially in a rapidly changing global economy. The reliance on historical data also means that economic models may fail to anticipate unprecedented events or structural shifts, further limiting their predictive utility.

Economic theories provide frameworks for loosely understanding complex market dynamics. They might offer some insights into the potential impacts of policies and decisions. However, the limitations of these models must be recognized. Economics, as it currently stands, lacks the precision and certainty that characterize the natural sciences. Its predictions are inherently uncertain, and its models are simplifications that can only approximate reality. Therefore, it is crucial to approach economic predictions with a healthy dose of skepticism and to be aware of the inherent uncertainties involved.

In Defense of The Economists

Defenders of economics as a science often argue that, despite its predictive challenges, economics provides invaluable frameworks for understanding market behavior and guiding policy decisions. They point out that economic theories have successfully explained various phenomena and have been instrumental in shaping effective policies. For example, the principles of supply and demand, market equilibrium, and comparative advantage are foundational concepts that have proven useful in both microeconomic and macroeconomic contexts. These same defenders assert that the utility of economic models, even if imperfect, justifies their status as scientific tools.

However, I would contend that the explanatory power of these economic frameworks is superficial and often akin to the behaviors observed in chimpanzees, which, while interesting, do not provide deep insights into human economic behavior. The theories often fail to account for the complexities and irrationalities inherent in real-world markets. For instance, the assumption of rational behavior is frequently contradicted by the unpredictable and often seemingly irrational actions of consumers and investors. Behavioral economics has highlighted numerous cognitive biases and emotional factors that significantly influence economic decisions, which traditional models typically overlook.

Another common defense is that economics, like any evolving science, is constantly improving its models and methodologies. Proponents argue that advancements in data collection, computational power, and interdisciplinary approaches are enhancing the accuracy and relevance of economic predictions. They highlight the growing integration of behavioral insights, machine learning, and big data analytics in economic research as evidence of the field's progression. While these advancements might indeed promising, they often do not address the fundamental issue of the non-linear and emergent nature of economic systems, which continues to elude precise prediction and control.

From where I’m sitting, it is essential to recognize that the incorporation of new methods and data does not necessarily resolve the core limitations of economic models. The reliance on historical data and the simplification of complex interactions remain significant obstacles. The field's tendency to retrofit explanations after events occur, rather than accurately predicting them beforehand, further undermines its claim to scientific rigor. Moreover, the frequent failures of economic forecasts during critical moments, such as financial crises and recessions, reveal the limitations of even the most advanced models. These shortcomings suggest that, while economics can offer useful notions and tools, its status as a predictive science remains dubious.

While defenders of economics as a science present valid points about its utility and ongoing advancements, the fundamental challenges of prediction in complex, non-linear systems cannot be ignored. The superficiality of many economic theories, the overreliance on simplified models, and the field's limited predictive success call into question its scientific rigor. Recognizing these limitations is crucial for developing more robust and adaptive approaches to economic analysis and policy-making, and for maintaining a realistic perspective on what economics can achieve.

Conclusion

In looking at the predictability of complex systems, we have exposed the intricacies of both natural and economic phenomena. Complex systems, characterized by their sensitivity to initial conditions, non-linearity, and emergent properties, present significant challenges for prediction and ultimately external control. From simple weather patterns to global warming and economic markets, the inherent unpredictability of these systems underscores the limitations of current predictive modeling aproaches. Despite advancements in technology and methodology, the fundamental nature of complex systems remains a serious obstacle to achieving precise and reliable forecasts beyond the short term.

Economics, as a discipline, exemplifies the challenges associated with predicting complex systems. Although economic theories and models might provide valuable frameworks for loosely understanding market behavior, when it comes to guiding policy decisions they often fall short of the empirical rigor and predictive accuracy that define the natural sciences. The reliance on simplified assumptions, the variability of human behavior, and the non-linear interactions within economic systems all contribute to the field's inherent limitations. In turn, these limitations raise important questions about the scientific status of economics.

While defenders of economics argue for its utility and the ongoing improvements in the field, one must approach economic predictions with a healthy dose of skepticism. The superficiality of many economic theories and the frequent failures of economic forecasts highlight the need for a more nuanced understanding of what economics can and cannot achieve. Recognizing the limitations of economic models is essential for developing more robust and adaptive approaches to economic analysis and policy-making. It also helps to temper expectations and avoid the pitfalls of over-reliance on economic predictions.

Finally, when one understands the nature of complex systems one comes to realize the profound challenges of predicting outcomes in environments characterized by non-linearity, sensitivity to initial conditions, and emergent behavior. Economics, as a field that deals with such systems, should certainly attempt to better grapple with these challenges and acknowledge its current limitations. While economic theories and models may offer valuable insights, their predictive power remains constrained by the complexities of the real world. In short, embracing a more humble and realistic perspective will be essential for making informed decisions in an increasingly unpredictable world.

All of this to say, focus on the short term. People around the world are suffering from issues that are solvable. For example, potable drinking water is essential for life. There is no reason (other than regional politics) why we cannot ensure that every human has access. We can do this right now. We don’t need to wait for the turn of the next decade or century.

Assume nothing. Take short term actions. Look at the outcomes. Make immediate adjustments. Measure again. Rinse, wash, repeat. It means being willing to say “I don’t know” when it comes to attempts to “manage” complex systems. It is the opposite of what traditional approaches to “knowledge” and modeling look like.

A week in Kauai would help :). If you have a layover in Honolulu at any point let’s grab lunch - the airport’s easy to get to.

Alex, my primary question is: how to you have time to create these treatises?

I am familiar with most of what you describe, and generally have come to similar conclusions. So while not a lot may be new to me, I definitely feel you’ve synthesized key insights from a number of fields and how they triangulate on issues including very topical ones. Synthesis like this takes real time to write… how do you balance your day such that the time needed exists?